The Insurance Commission (IC) jump started 2024 by intensifying efforts in eradicating unsound business practices in the Health Management Organization (HMO) sector. Spearheaded by Circular Letter No. 2024-01, this initiative introduces comprehensive guidelines aimed at defining and penalizing unsound business acts. Since the transfer of jurisdiction from the DOH to the IC, the Guidelines Defining Unsound Business Acts and Providing Administrative Fines for Violation Thereof (the “Guidelines”) must be one of the most significant steps the Commission has taken in its policy to protect the interests of healthcare consumers nationwide.

SCOPE AND APPLICABILITY

The Guidelines exclusively address unsound business acts of HMO and HMO Intermediaries.

An HMO is defined as “a juridical entity legally organized to provide or arrange for the provision of pre-agreed or designated health care services to its enrolled members for a fixed pre-paid fee for a specified period of time. While HMO Intermediaries “include HMO agents, brokers, and soliciting official under Circular Letter No. 2022-09”.

The Guidelines exclude those that affect compliance with requirement on capital adequacy, product approval, corporate governance, or other internal matters not directly dealing the public.

UNSOUND BUSINESS ACTS

The Guidelines identify several unsound business acts, including:

1. Misrepresentation to the public regarding HMO product provisions, payment of claims, and advertisement.

2. Unfair discrimination based on race, offering less advantageous rates or benefits to specific nationalities.

3. Unfair claims/availment management which includes surface bargaining.

4. Misrepresentation in HMO applications or through false statement or representation in reference to any HMO application.

5. Failure to effectively control and supervise its agent(s) by not establishing reasonable standards of supervision and control.

6. Failure to provide a copy of the HMO product, including all its riders and/or endorsements.

7. Failure by the HMO to respond to regular inquiries, directive, or order made by the IC.

8. Other analogous unsound acts which imply that the list is not exclusive, and that the Commissioner has discretionary powers to determine whether the conducts in question are indeed unsound business acts for purposes of preventing fraud or injury and protecting the rights of a member.

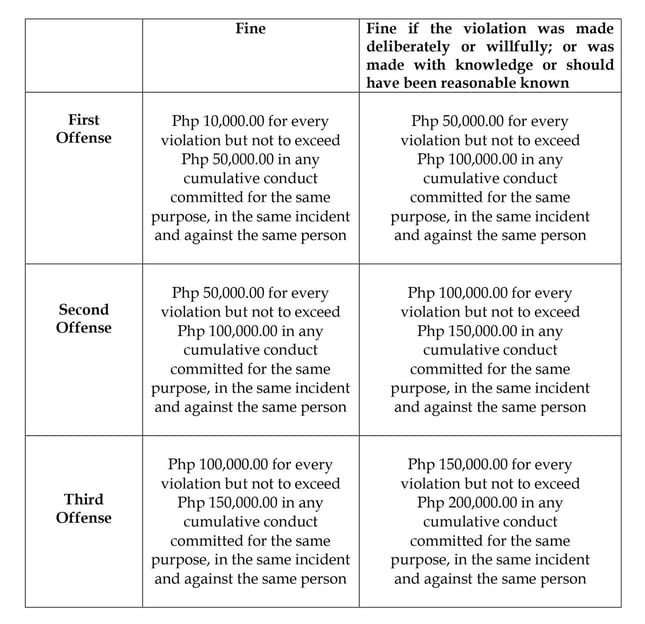

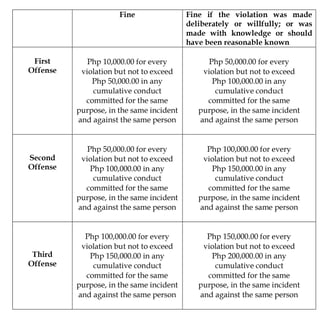

PENALTIES

A person found to have engaged in unsound business acts shall be meted with the following fines: